Turning retirement dreams into financial reality: Timeless strategies that can help your savings grow

The freedom to enjoy life on your own terms, with plenty of time (and money) to travel, focus on your hobbies or do whatever your heart desires may come to mind first when you think of retirement. But funding this milestone in one’s stage of life takes planning, discipline, and perseverance – and the sooner you start, the better.

How much do I need?

When building a retirement nest egg, there’s no hard and fast rule about how much you should save. The amount ultimately comes down to the type of lifestyle you hope want to enjoy when the days of earning a regular paycheck are over. A good place to start is mapping out your current expenses and making an educated estimate about the projected cost of living in your senior years. For instance, during this time, you may no longer have mortgage payments or child-care expenses, and your grocery budget may shrink if your kids move out. You may have big plans that require financial foresight, like enjoying regular vacations or purchasing a luxurious car.

When considering retirement expenses, it’s helpful to drill them down to two categories:

- Basics

- Non-essentials

Basics refer to things you can’t live without, such as groceries, housing, healthcare, transportation, gas, and, yes, insurance. The price of many basics will depend on where you plan to live in your retirement. If you plan to move, calculate the difference in cost of living.

Non-essentials are the fun things you want to do in retirement, such as eating out, joining a club or pursuing hobbies, forms of entertainment and other leisure activities.

Understanding the magic of compound interest

Retirement may feel like decades away, but the sooner you start saving, the better prepared you’ll be to enjoy your future. To make the most of your savings, it’s important to understand the power of compound interest. In simple terms, as the interest you earn is reinvested, it helps your savings grow faster over time.

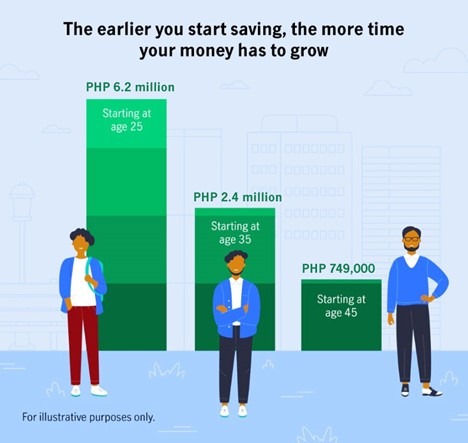

Let’s look at the effects of compound interest on an annual contribution of PHP 40,000 to a retirement plan, assuming you’ll retire at age 60 and the investments earn 8% compounded yearly.

- If you start saving at age 45, then you’ll have saved just almost PHP 750 thousand.

- If you start saving a bit earlier, say age 35, then you’ll manage to save more than thrice.

- If you begin saving for retirement at age 25, you can save almost PHP 6.2 million.

Note: Sample benefits for a male aged 25, 35 and 45, paying PHP 40,000 per year, up to the target retirement age of 60 years old for a PHP 1.8 million Face Amount, assuming an 8% fund growth rate.

Retirement ready?

Ask yourself these questions to help in the planning process:

- When do you want to retire? Knowing at what age you’ll step back from the workforce can help you determine how many years you’ll be saving for.

- Where will you retire? Whether you plan to relocate to another city, stay in the family home, downsize to a condo or rent will have a big impact on the size of the retirement nest egg you may require.

- Do you plan to continue working? Maybe your idea of retirement is easing back from full-time hours to a more relaxed and fun part-time job. For many, a job offers a sense of purpose, structure, and belonging that boosts not only your vitality but also your bank account.

- How will you spend your time? Downtime may seem idyllic if your working life has been hectic all this time, but too many idle hours make for long days. Think of how you aim to occupy yourself. It might be spending more time with family, travelling or volunteering for a good cause.

- How might your health affect your spending needs? You may be healthy now, but it’s important to plan for potential what-ifs down the road. Consider the impact of therapies, mobility supports and assisted living on your retirement budget.

Start Building Your Retirement Plan with Manulife’s FutureBoost Retirement

There’s no perfect time like the present to save for your future! Manulife’s financial advisors can help determine the best options available based on your household budget, peak earning years and risk tolerance.

Manulife FutureBoost Retirement is a powerful solution to go beyond savings and pension for your retirement. By combining the benefits of life insurance with potential for wealth accumulation through expertly managed funds, this plan provides you with the tools to secure your financial future. In addition, as global and local economies continue to evolve, FutureBoost Retirement can help protect you in the present, while preparing for a comfortable retirement.

Let us help build your future with FutureBoost Retirement. Talk to us to learn more.

If you liked this article, you may find these interesting

Thank you, {FirstName}, for sharing your contact details with Manulife!

We will be contacting you to talk about your inquiry.

Oops! There seems to be a problem.

Please review the form and make sure you filled out all the necessary details.

-

Enjoy a Better Life with These 5 Financial Tips

Read moreAll kinds of goals—whether short-term or long-term, require smart saving and financial security. Here are a few ways to save money while enjoying life!

-

Guaranteed Savings for Your Long-term Goals

Read morePlanning for our dreams can be complicated and overwhelming. Defining your short-term and long-term goals is essential to achieving success and personal satisfaction.

-

8 Ways To Be More Money-Smart

Read moreWant to be better with your finances? The earlier you start working towards being more money-smart, the sooner you can achieve your financial goals.

Manulife Philippines is regulated by the Philippine Insurance Commission and is authorized to provide financial products or services in the Philippines.

Copyright © 2020, The Manufacturers Life Insurance Company and its subsidiaries. All rights reserved. Main office: 10th Floor NEX Tower, 6786 Ayala Avenue, Makati City, 1229 Tel : +632 8884 7000, Toll-free: 1-800-1-888-6268